This proposal seeks approval to integrate PT-eUSDe-29MAY2025 as collateral on the Euler Yield market. We believe this will allow Euler DAO to strategically expand its competitive stablecoin yield offering, capture current demand for eUSDe, and stimulate mutual growth with Ethereal.

Motivation

eUSDe is the receipt token of the pre-deposit vault of Ethereal, the flagship spot and perp DEX on Ethena Network. PT-eUSDe is currently the most liquid pool on Pendle (~$150M) with implied yield at ~12%. Euler is enrolled in Ethereal’s points program with competitive terms for both eUSDe and PT-eUSDe deposits.

Risk

In addition to the risks of eUSDe as identified by Gauntlet and Objective Labs, we believe the PT token does not add further material risks. Pendle smart contracts are thoroughly battle-tested by time and TVL. PT-eUSDe is the most liquid pool on Pendle. Pre-deposited eUSDe is instantly withdrawable 1:1 to USDe, making for a highly liquid path from PT to any stablecoin. Finally, Euler Yield hosts only USD-derivative assets, so we do not expect liquidations to happen in the normal case.

Caps

Supply Cap

Borrow Cap

5M (~$5M at expiry)

0 (borrowing disabled)

Objective Labs recommends that PT be non-borrowable in line with strategy for PTs.

Liquidation LTVs

Debt

LLTV

wM

82%

USDT

82%

USDS

82%

USDe

90%

eUSDe

90%

USDC

82%

USD0

82%

RLUSD

82%

PYUSD

82%

FDUSD

82%

DAI

82%

In line with the rest of the market, Objective Labs recommends that the borrow LTV should be set to two percentage points less than liquidation LTV.

Interest Rate Model

The IRM can remain unset since PT-eUSDe will be non-borrowable.

Oracle

We propose that a Pendle PT market oracle be used, crossed by eUSDe’s ERC4626 conversion rate, crossed by Pyth USDE. The latter part of the same oracle configuration matches the one used for eUSDe.

Author

Objective Labs is a service provider for Euler Labs tasked with product development, risk management, and incentive optimization. Objective Labs is Euler-aligned.

Hey @Objective, eUSDe as a loan asset against PT looks very cool, but it’s inactive to borrow. What risk-recommendations would you consider (irm, borrow cap and oracle)?

[Gauntlet] Parameter Recommendations for PT-eUSDe-29MAY2025 on Euler Yield (2025-03-28)

In light of the proposal by Objective Labs, Gauntlet recommends the following risk parameters to the protocol:

Cap Recommendations

Gauntlet will recommend this asset is not initially borrowable given its limited such utility as a maturing PT.

Set supply cap to 40,000,000

Set borrow cap to 0

Presently PT-eUSDe can withstand over 50M swap to SY-eUSDe in Pendle AMM with less than 1.5% price impact. Subsequent rationale follows that in our 03/27 proposal for updating the eUSDe supply cap.

We are aligned with the risk profile of the oracle recommended by Objective Labs. Using a Pendle PT oracle would continually allow the PT-eUSDe / eUSDe price to converge to market price based on implied APY and tenor within reasonable time.

Interest Rate Curve Recommendations

This asset is recommended to not be borrowable initially, so no IR curve need be set.

LLTV Recommendations

Here we aim to maximize risk-adjusted capital efficiency for users. We anticipate usage of markets for looping PT-eUSDe / stablecoins, PT-eUSDe / eUSDe, and PT-eUSDe / USDe.

This table assumes PT-eUSDe as the collateral asset.

Borrow LTVs are recommended as four percentage points less than the recommended LLTVs per collateral/debt pair.

Debt

LLTV

wM

86%

USDT

86%

USDS

86%

eUSDe*

92%

USDe

90%

USDC

86%

USD0

86%

RLUSD

86%

PYUSD

86%

FDUSD

86%

DAI

86%

eUSDe Borrow Recommendations*

As pointed out by @daffy, borrowing is not currently enabled for eUSDe. As part of the recommendations for this asset, we also recommend enabling eUSDe borrows.

Cap Recommendations

We recommend setting the borrow cap to 50% of the supply cap (which our current proposal recommends at 40M). Borrowing demand will be expected for PT-eUSDe / eUSDe looping. We would like to support capital efficiency while noting heavy usage of eUSDe as collateral for looping eUSDe / stablecoin positions. Therefore borrowing should be limited to the extent that sufficient redemption capacity will exist for liquidators during long tail events.

Interest Rate Curve Recommendations

Since mid-February, Pendle implied APY for eUSDe has decreased from 17.9% to 11.3%. Noting this trend, we recommend the following IRM:

Objective Labs is proposing to onboard the new 14 Aug maturity for PT-eUSDe in Euler Yield.

With the previous PT maturing in 12 days, we expect borrowers to switch over to the new maturity over the next week. Liquidity for the new maturity is already at 32M. Implied yield is slightly higher due to the new maturity having 1.6x Ethereal multiplier rather than 1x.

We are recommending to use of the same LTV configuration as the May maturity PT with an initial supply cap of 60M.

[Gauntlet] - PT-eUSDe-14Aug2025 Review and Recommendations

Summary

Gauntlet has reviewed Objective Labs’ proposal to onboard PT-eUSDe-14AUG2025 and supports the recommendation to proceed with listing the new August maturity on Euler Yield. We agree with maintaining the same LTV setting and recommend the initial supply cap at 70M to accommodate expected demand and rollover activity.

Rationale:

Low Risk Profile: The proposed maturity inherits the same structural characteristics and underlying risk as the May maturity, which has performed without incident. Gauntlet assesses the borrower and protocol risk to be low.

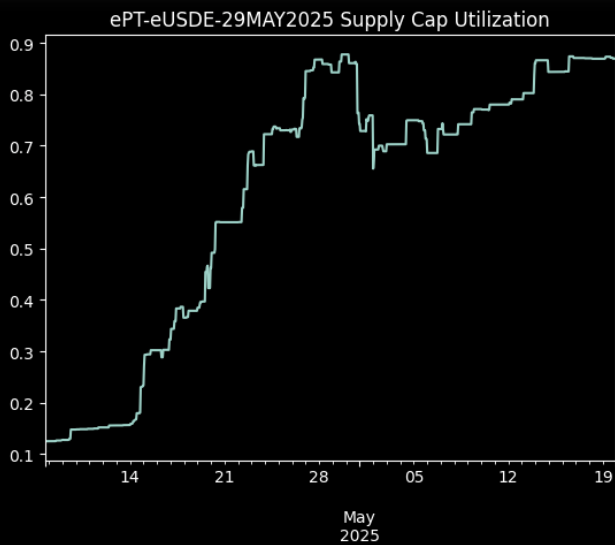

Current Supply Cap Utilization

Supply cap utilization for PT-eUSDe-29MAY2025 has reached approximately 90%, underscoring strong market demand for this maturity. With the current supply cap set at 45M, the rapid uptake reflects sustained activity around this primitive.

In anticipation of continued demand and to support a smooth transition as the 29MAY maturity approaches expiry, we recommend setting the initial supply cap for PT-eUSDe-14AUG2025 at 70M (~1.5x of the current cap). This higher cap is intended to accommodate rollover activity from the maturing tranche, as well as additional organic growth driven by the enhanced Ethereal multiplier and attractive implied yield profile of the new maturity.