Summary

This post proposes a unified oracle policy across Euler DAO-governed markets to improve liquidation fairness, reduce desynchronization risk across derivative-underlying pairs, and standardize provider choices by asset class and market behavior. The Oct 10 market stress event provided clear evidence regarding provider behavior and update cadence that informs these recommendations.

Policy

1. Derivative-underlying pairs: use coincidental price feeds

Within a given market, derivatives and their underlying assets must share the same price feed for the common underlying component.

Example

PT-pUSDe and USDe both read the same USDe/USD oracle.

Rationale

Eliminates oracle desynchronization between derivative and underlying legs, reducing liquidation unfairness during fast markets. Prior Euler guidance already stressed migrating entire asset families to the same underlying feed to avoid desync. See Modify Euler Yield's configuration to facilitate EulerSwap pools

2. Market price feeds for correlated pairs: prefer RedStone over Chainlink

For correlated assets with lower liquidity or cross-chain exposure, prioritize RedStone oracle feeds over Chainlink to reduce stale-quote risk during volatility.

Example

Prefer RedStone USDe/USD rather than Chainlink USDe/USD.

Rationale

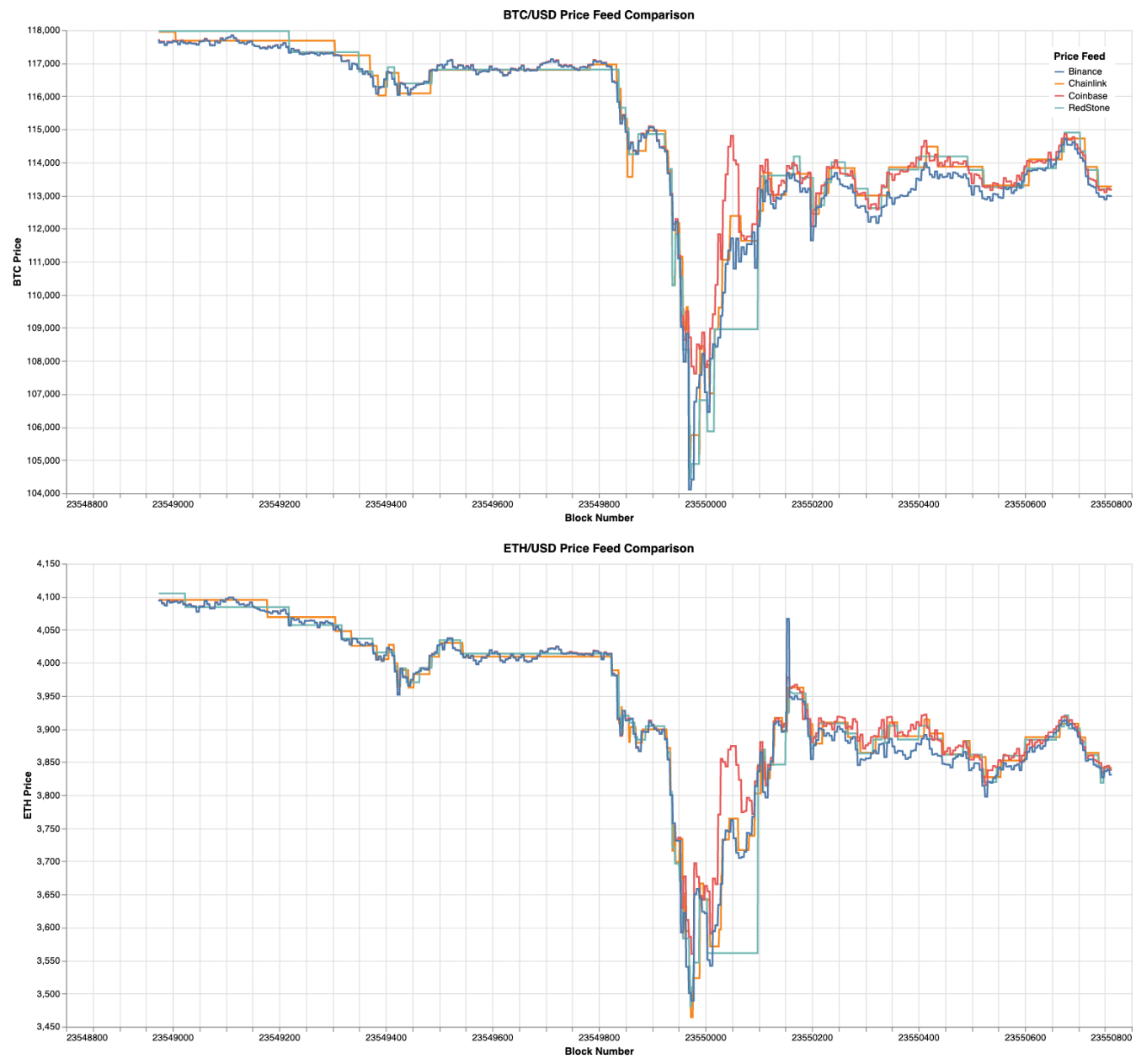

Chainlink’s VWAP methodology and deviation-based push updates can underperform on thin or low-correlation asset pairs, creating transient mispricings and wrongful liquidations (e.g., the deUSD event on Avalanche). For correlated assets with lower liquidity or venue dispersion, RedStone’s tighter deviation thresholds (0.2% vs 0.5%) and faster update cadence reduce stale-quote risk. During the Oct 10 stress event, RedStone delivered faster, more granular price updates.

3. Major volatile pairs: use OEV-enabled price feeds

Pilot RedStone Atom for ETH/USD and BTC/USD.

Rationale

OEV aligns update rights with value capture during liquidations, increasing update frequency and reducing stale prices at the margin. Prior Euler research noted that granularity limits of deviation-threshold updates degrade Dutch auction efficiency. OEV-integrated updates can bypass thresholds and unify the price and blockspace auctions to reduce leakage and improve liquidation fairness. Both Chainlink (via SVR) and RedStone (via Atom) made faster, more granular updates with OEV enabled during recent stress periods.

ETH/USD and BTC/USD are the logical starting points: these are the most popular oracle feeds across DeFi, ensuring the largest and most competitive searcher networks will actively participate in OEV auctions. Additionally, we expect the majority of liquidations on Euler to flow through ETH- and BTC-denominated collateral pairs, making these feeds the optimal risk-reward choice for piloting OEV integration. Our independent evaluation of Chainlink and RedStone OEV solutions concluded that RedStone Atom’s architecture offers marginal advantages over Chainlink SVR in latency and granularity, although Chainlink’s solution benefits from greater battle-testing through its Aave integration.

4. Fundamental feeds: prefer onchain rate over oracle provider

For exchange-rate and fundamental assets (LSTs, ERC-4626 vaults, rate providers), use onchain rate functions rather than externally-sourced price feeds.

Example

weETH uses EtherFi’s onchain fundamental weETH/ETH rate rather than an oracle-provided weETH/ETH. ERC-4626 vault shares use the vault’s convertToAssets() method where manipulation-resistant.

Rationale

Onchain rate functions eliminate congestion-induced push/pull latency and reduce unnecessary transport-layer risk. For assets with direct, manipulation-resistant onchain redemption or exchange rates, querying the source protocol is more reliable than introducing an external oracle intermediary.

5. Pendle PT feeds: prefer custom/hybrid oracle over pure TWAP

For Pendle Principal Tokens (PTs) and similar derivative structures, prefer custom oracles engineered for these assets rather than a pure market TWAP.

Rationale

Pendle’s AMM has a built-in trading range that enforces a minimum PT price floor. During market stress, when traders dump PT positions, the implied APY spikes (as PT price drops). In this scenario, the PT can trade below the AMM’s minimum price on external orderbook venues while the AMM itself remains pinned at the floor. A pure TWAP oracle observing only the Pendle pool would overprice the PT relative to its true market value, creating liquidation risk for borrowers and bad debt exposure for lenders. Custom oracles that account for this failure mode, such as hybrid PT feeds, can avoid this pricing gap during crashes.